- Base Value(2025): 1663 Mn

- Forecast Value (2035): 3211 Mn

- CAGR (2035): 6.8%

Ready-to-Eat Wet Soup Market Outlook (2025 to 2035)

The global Ready-to-Eat Wet Soup Market is expected to reach USD 3,211 million by 2035, up from USD 1,562 million in 2024. During the forecast period from 2025 to 2035, the industry is projected to expand at a CAGR of 6.8%.

The ready-to-eat wet soup market is gaining traction as consumers increasingly seek convenient, nutritious, and flavorful meal solutions. With the rise of urban lifestyles, busy schedules, and a demand for shelf-stable yet fresh-tasting products, wet soups offer an ideal balance of health and convenience. Innovations in packaging, clean-label formulations, and global flavor profiles are making these soups a popular choice across diverse demographics.

| Metric | Value |

|---|---|

| Industry Size (2025E) | USD 1,663 million |

| Industry Value (2035F) | USD 3,211 million |

| CAGR (2025 to 2035) | 6.8% |

What are the drivers of the Ready-to-Eat Wet Soup Market?

The market for ready-to-eat wet soup is experiencing notable growth, largely influenced by changing consumer dieting patterns and the rising popularity of convenience-oriented meals. Urban dwellers, particularly in developed economies, are increasingly seeking time-efficient food options that do not compromise on taste or nutritional value. To fulfill this demand, ready-to-eat wet soups are available due to their short preparation time, various flavors, and balanced nutritional status.

One feature that is significant to drive the market is the current infiltration of the trend into functional food. Consumers are shifting towards protein-enriched, fiber-enriched, probiotic, and immunity-strengthening soups. The value-added formulations are broadening the base of wet soups, which were earlier positioned as a comfort food, to include a part of a healthy lifestyle. In addition, the emergence of clean-label categories and allergen-free products has increased in appeal and confidence, especially among sensitive demographics such as children and the elderly.

Consumer interest is sustained through brand diversification, including seasonal and limited-edition flavor variants, as well as other high-quality, globally inspired produce. Moreover, the collaboration of food manufacturers with cloud kitchens is developing new distribution options for gourmet soup. The use of new food processing technologies, including high-pressure processing (HPP), enables the preservation of flavor while increasing safety by ensuring microbial safety, thereby enhancing product quality and fostering consumer trust in the category.

What are the regional trends of the Ready-to-Eat Wet Soup Market?

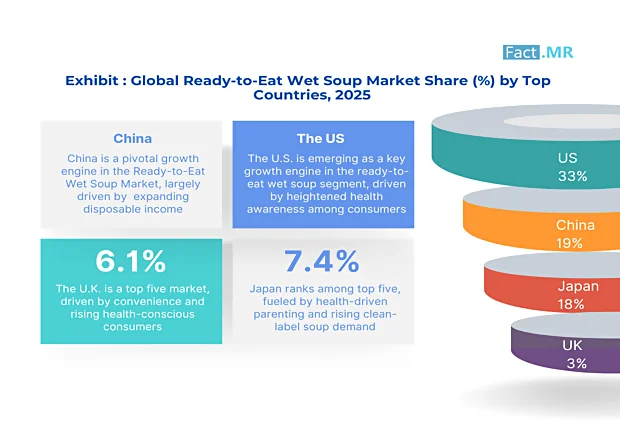

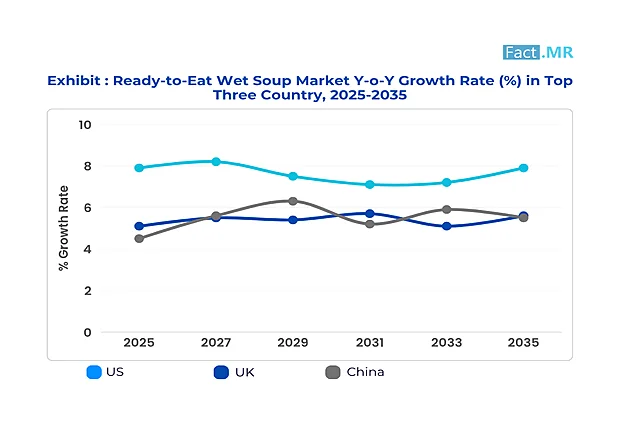

North America is a dominant market with a high level of product penetration in the retail and foodservice networks of the ready-to-eat wet soup market. Consumer preference in the US market, in particular, shows a high demand for artisanal and low-sodium formulas, with product development centered on organic and locally sourced ingredients. Comfort-food nostalgia-based marketing efforts are successfully being converted into repeat sales.

Matching product regulations with sustainable food systems influences product innovation in Europe. Higher demand for clean-label soups, including their plant-based variants, is observed in Scandinavian and Western European markets. Traceability and ethical sourcing are among the key factors that local brands are focusing on to meet the needs of environmentally conscious buyers. Another emerging trend across the continent involves incorporating soups into meal kits and subscription services.

The most dynamic landscape in the world is the Asia-Pacific region, where the rapidity of change in urban lifestyles and the increasing number of dual-earner families are expanding. The convenience of the wet soups is capturing the market not only among working adults, such as in South Korea and China, but also among students and the elderly. Regional adoption is also being boosted by the expansion of national brands that cater to local taste preferences.

Latin America and the Middle East are emerging as new demand zones. In Brazil and Mexico, the proliferation of organized retail and growing affinity for Western cuisine are facilitating market expansion. Meanwhile, Gulf countries are experiencing an increase in demand for premium hospitality and wellness-focused retail, particularly during fasting periods and health-driven dietary changes.

What are the challenges and restraining factors of the Ready-to-Eat Wet Soup Market?

The ready-to-eat wet soup market is faced with a unique set of challenges that may plausibly moderate its growth trajectory. Product differentiation in an oversaturated flavor market is one of the major concerns. With numerous brands offering similar core variants like tomato, mushroom, and chicken, achieving meaningful innovation without alienating traditional consumers becomes a balancing act.

The other constraint is thermo-sensitive supply chains. Preservative-free or organic wet soups that require high efficiency in their quality and safety standards are crucial for their preservation in cold chain systems. This brings about infrastructure and compliance requirements, particularly in emerging markets where refrigeration infrastructure is underdeveloped.

Consumer perception and shelf appeal also present a significant barrier. Even with the art of packaging, a taste bias for wet soups persists, correlating with a preference for institutional or processed food. Overcoming this stigma requires substantial branding efforts and sensory marketing to convey freshness and gourmet quality.

Moreover, there are variations in labeling, nutritional reporting and expiry dates of the products in different regions, which makes it more complicated to operate as a multinational brand. Adapting formulations and packaging for localized compliance slows down go-to-market strategies and introduces additional cost layers not through material input but through procedural overhead.

Country-Wise Insights

Functional Nutrition and Refrigerated Retail Reshape USA Preferences

In the USA, consumer interest in health-centric convenience is driving significant innovation in ready-to-eat wet soups. Soups are already being marketed as full meals, made with pre-cooked soups that include added protein, anti-inflammatory herbs, and probiotic-friendly ingredients. The most notable demand is by urban consumers who are keen on wellness, requiring fast foods that are not detrimental to dietary objectives.

Retailers are expanding refrigerated zones to include fresh soup items with limited ingredients and without preservative components. This trend is especially evident in organic grocers and DTC outlets, where meal prep fatigue has sparked renewed demand for microwave-ready, clean-label solutions.

FDA oversight on sodium, sugar, and allergen labeling is prompting transparent formulations. However, consistent nationwide cold-chain execution remains a challenge, especially for small to midsize producers looking to scale beyond local markets without compromising freshness or taste.

Regional Ingredients and Portable Packaging Spark UK Momentum

UK consumers are adopting ready-to-eat soups with a homegrown culinary identity and the natural origin of ingredients. The new versions, based on heritage with British-grown vegetables and meat, have been gaining popularity as companies utilize regional brand narratives to enhance authenticity and differentiate their offerings.

Innovations in transportation are influencing the trend in packaging, where convenient and small, easy-to-reheat packaging is becoming the favorite of busy urban workers. These soups are increasingly merchandised in grab-and-go sections of convenience stores and transportation hubs, reflecting the growing demand for hot, balanced meals on short notice.

Reformulation pressures tied to national salt reduction campaigns are influencing the development of cleaner recipes. A structural limitation persists in rural areas, where access to premium or specialty offerings remains limited, as supermarket assortments in smaller towns tend to be skewed toward less differentiated, ambient options.

Tradition Meets Technology in China’s Expanding Soup Segment

China’s market is blending centuries-old culinary practices with modern convenience through digitally distributed, pre-cooked wet soups. Formulations draw on TCM traditions, utilizing ingredients such as jujube, astragalus, and chicken essence, to offer perceived benefits for immunity and vitality in ready-to-heat formats.

Livestream commerce and algorithm-driven product bundles are pushing innovative launches into lower-tier cities. Bowls with sealed freshness locks and reheating indicators are designed for workplace dining and late-night consumption, supporting around-the-clock demand in densely populated urban zones.

Government mandates on ingredient disclosure and traceability are helping to build consumer trust in emerging domestic brands. The key challenge lies in preserving the depth of traditional flavors within automated, scalable systems that cater to rapidly changing consumer preferences without compromising quality.

Category-Wise Analysis

Tomato-Based Wet Soups Anchor Product Familiarity and Category Entry

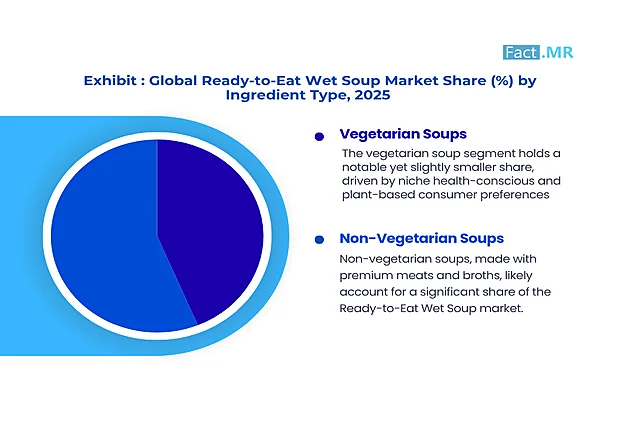

The use of tomatoes in soup has sustained the vegetarian category of ready-to-eat wet soup portfolios, as it retains a cross-regional acceptability factor and is easy to formulate. Tomatoes feature a natural acidic profile, which presents in-built preservation benefits, making them less reliant on chemical stabilizers. It is also most often chosen in the first product releases due to its widespread nature and compatibility with different flavor systems, such as basil, garlic, lentils, and dairy.

Producers are experimenting with a combination of tomato bases, incorporating high-protein grains or legumes, which aim to satisfy hunger without compromising the palatability of the food. Production-wise, it is easy to obtain tomato concentrates through global supply chains, thereby ensuring the consistency of tomatoes throughout the year.

In foodservice environments, tomato-based soups are favored for their speed of service and flexibility in reconstitution. The segment also benefits from strong promotional elasticity, often featured in bundled meal kits or seasonal offerings. With the health-conscious consumer still focusing on simple and recognizable ingredients, tomatoes remain a dominant factor in the volume-driven category, influencing repeat buying behavior.

Canned Packaging Gains Preference on Cost-Efficiency and Unit Economics

Canned packaging maintains its strategic advantage in the wet soup market, driven by optimized fill-to-cost ratios and strong supply chain handling. Canning lines support high-throughput production with minimal per-unit variance, reducing operating costs for both manufacturers and distributors.

The format offers natural protection against the spread of microbes, complemented by heat-based sterilization methods that eliminate the need for preservatives. High-acidic contents, such as tomato and mushroom-based soups, are also packaged using cans, whose material compatibility guarantees the stability of the product.

The firm packaging minimizes the floor space required in the transportation sector, and prolonged shelf stability minimizes product waste for sale in retail and food service settings. Branding has evolved with direct-on-metal printing, enabling the differentiation of products even in established retail environments.

In emergency preparedness and institutional foodservice, cans remain the preferred means of food storage due to their ability to store food over long periods without refrigeration. While recyclable features add peripheral sustainability value, the primary driver of adoption remains cost containment, particularly in value-tier SKUs and government-supplied nutrition programs.

Organic Wet Soups Reflect Evolving Premiumization Dynamics

Organic wet soups also mark an important shift in consumer demand towards transparent, clean attributes and health-conscious food products. This segment is also expanding beyond its niche specialty aisles and into mainstream distribution channels as organic certification standards become increasingly recognized and reliable. Direct sourcing and contract farming are becoming immensely popular in food production as they allow their producers to uphold the integrity of their supply and the integrity of the ingredients they use.

The ingredients used in the formulation of products in this category favor a few, unrefined ingredients, sometimes incorporating heritage vegetables or low-glycemic grains to cater to consumers concerned with wellness. The non-use of synthetic fertilizers, pesticides, and genetically modified organisms makes organic soups compliant with regulatory and voluntary standards in several jurisdictions. Shelf-stable organic lines are further gaining appeal among consumers seeking convenience without compromising on dietary values.

The segment’s momentum is also tied to the rise in functional health claims, particularly in relation to gut health and detoxification. As consumer sophistication evolves, organic soup SKUs are expected to expand in both variety and average unit price.

Competitive Analysis

Key players in the ready-to-eat wet soup industry include Campbell Soup Company, The Kraft Heinz Co., General Mills Inc., Hain Celestial Group Inc., Amy's Kitchen Inc., Baxters Food Group Limited, Princes Limited, Conagra Brands, Inc., Trader Joe's Ltd, Tideford Organic Foods Ltd, Pea Soup Andersen, and J Sainsbury PLC.

The growth of this market is driven by the increasing demand for convenient, shelf-stable food that meets the diverse needs of consumers' varying lifestyles. Healthy lifestyles, urbanization, and growing consumer preferences for heat-and-eat meals are providing steady expansion opportunities. The competitive forces are also being influenced by clean-label trends, plant-based innovation, and the premiumization of their traditional soup offerings.

Companies are responding with differentiated formulations, organic and vegan variants, and eco-conscious packaging solutions. Private-label expansion, strategic collaborations with retailers, and investments in regional taste profiles are further enhancing market competition. Responsible sourcing, less sodium, and packaging in renewable formats are other ways that players are adopting sustainability.

Recent Development

- In November 2024, Amy’s Kitchen launched five globally inspired organic soups, blending bold international flavors with clean ingredients. Varieties like Thai Coconut and Mexican-Style Black Bean reflect diverse culinary traditions. These ready-to-serve soups cater to consumers seeking convenience, global taste experiences, and USDA-certified organic, plant-based nourishment.

- In August 2024, Campbell’s Foodservice expanded its Culinary Reserve portfolio with globally inspired soup flavors, including Coconut Chicken & Lemongrass and Spicy Vegetable Ramen. Developed for chefs seeking premium, versatile ingredients, these soups combine convenience with bold international profiles, reflecting the evolving tastes of consumers and the culinary creativity in foodservice operations.

Fact.MR has provided detailed information about the price points of key manufacturers of the ready-to-eat wet soup market positioned across regions, sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

Fact.MR’s 2025 global ready-to-eat wet soup market report is based on responses from over 10,000 stakeholders across more than 30 countries, with a minimum of 300 participants per country. Approximately 70% were end-users or producers, including soup manufacturers, foodservice providers, and grocery chains. The remaining 30% consisted of industry professionals, including supply chain managers, chefs, and distributors.

Data collected from June 2024 to May 2025 covered market trends, demand, investments, unmet needs, and risks. Responses were weighted to match regional market sizes and demographics.

The report also draws on insights from more than 250 sources, including academic journals, patents, regulatory filings, and financial documents. Statistical methods, including regression analysis, were employed to enhance accuracy.

Fact.MR has tracked industry trends, consumer behavior, and market opportunities since 2018, making this report a reliable resource for global stakeholders.

Segmentation of Ready-to-Eat Wet Soup Market

-

By Ingredient Type :

- Vegetarian Soups

- Tomato

- Mushrooms

- Potato

- Onion

- Broccoli

- Corn

- Other ingredients

- Non - Vegetarian Soups

- Chicken

- Beef

- Sea Food

- Other ingredients

- Vegetarian Soups

-

By Packaging Type :

- Bottles

- Cans

- Packets

-

By Nature :

- Organic

- Conventional

-

By Sales Channel :

- HoReCa

- B2C

- Modern Trade

- Online Stores

- Drug Store

- Departmental Stores

- Convenience Stores

- Other

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Ready-to-Eat Wet Soup Market Size Reported by Fact.MR for 2025?

The Global Ready-to-Eat Wet Soup Market was valued at USD 1,663 million in 2025.

Who are the Major Players Operating in the Ready-to-Eat Wet Soup Market?

Prominent players in the market are Campbell Soup Company, The Kraft Heinz Co., General Mills Inc., Hain Celestial Group Inc., among others.

What is the Estimated Valuation of the Ready-to-Eat Wet Soup Market in 2035?

The market is expected to reach a valuation of USD 3,211 million in 2035.

What Value CAGR did the Ready-to-Eat Wet Soup Market Exhibit Over the Last Five Years?

The historic growth rate of the ready-to-eat wet soup market was 6.1% from 2020 to 2024.