- Base Value(2025): 122.1 Bn

- Estimated Value(2026): 129.2 Bn

- Forecast Value (2036): 213.2 Bn

- CAGR (2026 - 2036): 5.2%

Bio-Feedstock Market Outlook (2025 to 2035)

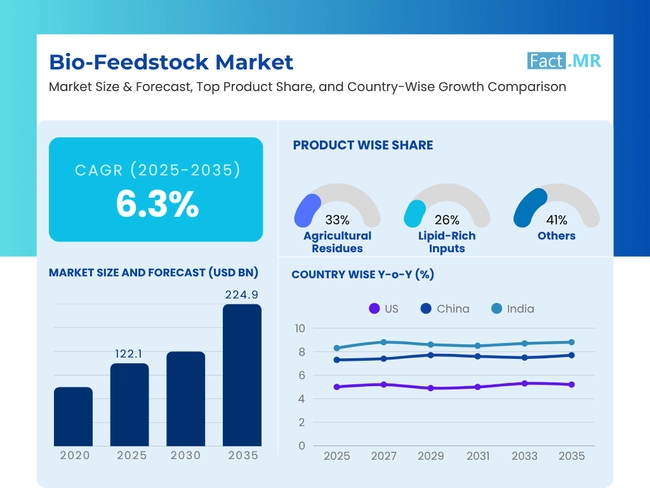

The global bio-feedstock market is expected to reach USD 224.9 billion by 2035, up from USD 115.0 billion in 2024. During the forecast period from 2025 to 2035, the industry is projected to expand at a CAGR of 6.3%, as the market emerges to meet the growing demand for sustainable raw materials in various industries.

It is crucial to decarbonize fuel production, plastic, and chemical manufacturing by transitioning from fossil-based feedstocks to renewable biomass, waste oils, and agricultural residues. The reason behind this transformation is the impact of carbon regulations, green mandates, and circular economy ambitions in the transportation, packaging, and bio-refining sectors.

What are the drivers of the Bio-feedstock Market?

The mixture of environmental, regulatory, and technological considerations drives the bio-feedstock market. One of the main factors is the global focus on sustainability and the need to mitigate greenhouse gas emissions. Strict carbon regulations, such as the EU Renewable Energy Directive (RED II), the USA Renewable Fuel Standard (RFS), and the California Low Carbon Fuel Standard (LCFS), among others, are being drafted by governments, which require an increase in the use of renewable and low-carbon feedstocks.

Refining, enzymatic conversion, and fermentation technologies have increased the feasibility and profitability of bio-feedstock production, thereby enhancing its use in biofuels, bio-plastics, and bio-chemicals. Switching to waste-derived and non-food-based feedstocks, such as agricultural residues, municipal waste, algae, and others, which also meet the sustainability criteria, increases the accessibility of feedstocks.

The increased demand for bio-feedstock in support of the sustainability of sustainable aviation fuels (SAF), renewable diesel, and low-carbon consumer products by major industries is also a confirming factor for the growth of bio-feedstocks. In addition, more investments by businesses in circular economy approaches and supply chain resiliency boost market momentum. A combination of these drivers makes bio-feedstocks key players in realizing global decarbonization and energy diversification goals.

What are the regional trends of the bio-feedstock market?

The trends in the bio-feedstock market are region-based, indicating varied policy frameworks, industry capacities, and availability. North America and USA In particular, regulatory requirements such as the Renewable Fuel Standard (RFS) and the Inflation Reduction Act (IRA) result in high demand of renewable feedstocks. The LCFS of California also offers a further incentive, namely, low-carbon alternatives, resulting in increased imports of used cooking oil (UCO) and investments in domestic feedstock production.

The emphasis in Europe is on an agenda of sustainability led by the Renewable Energy Directive II (RED II), which will limit food-based biofuels and promote the use of waste-based and non-edible feedstocks. Germany, France and the Netherlands are among the first countries to adopt circular economy policies as well as good refining infrastructure.

Bio-feedstock markets in the Asia-Pacific region are growing due to rapid industrialization and increasing energy demand. The countries such as China and India are investing in local biomass supply chains and refining capacity. Japan is also concerned with sustainable aviation fuel (SAF), and tests have been carried out using non-edible oilseeds. Generally, environmental policies, energy requirements, and the extent of bio-based industrial ecosystems determine regional dynamics.

What are the challenges and restraining factors of the bio-feedstock market?

The bio-feedstock market faces several difficulties and limiting factors that may negatively impact its development. Feeding living creatures availability and competition is a serious problem; bio-feedstocks frequently compete with food and feed applications, bringing about durability and morality issues. This is especially true for crops such as corn, soy, and palm oil, which are widely used in the major food and fuel industries.

The constraints in the supply chain and the seasonal nature of supply further impact the stable supply of feedstock, whereas the use of imported raw materials, such as used cooking oil (UCO), introduces problems of traceability and price uncertainty. In addition, their processing and production costs, particularly for advanced feedstocks such as algae or lignocellulosic biomass, restrict their commercial competitiveness unless they are subsidized or encouraged through direct incentives (payments) or tax rebates.

The uncertainty of regulation also hinders growth, as changing carbon intensity standards, land use, and feedstock eligibility can introduce investment risk. Infrastructure constraints, such as the inadequacy of biorefineries or logistics networks, also exacerbate these issues. Together, these factors pose significant hurdles to scaling the bio-feedstock market in a sustainable and economically viable manner.

Country-Wise Insights

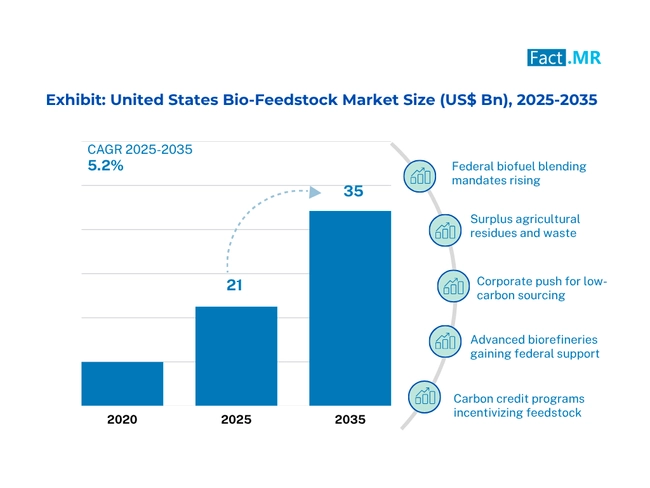

United States Edge in Bio-Based Innovation and Policy Support

The American bio-feedstock industry is driven by good federal policies such as the Renewable Fuel Standard and green energy requirements at the state level. Such frameworks create positive conditions for investing in biomass growth, research, and development, as well as biorefinery development, in the thriving areas of the Midwest and the Pacific.

Public-private partnerships in research add weight to technological advances, particularly in cellulosic ethanol and algae-based oils. Economic and Environmental feasibility is also on the rise due to the improvement of waste-to-energy techniques, making the USA one of the leaders in next-generation bio-feedstock systems.

The outlook for the US market is positive due to increased demand for biofuels and bioplastics, as well as sustainable agriculture. The sector is poised to expand robustly over the next 20 years, with infrastructure, investor confidence, and clarity of regulations boosting its growth.

China's Drive for Biomass Utilization and Circular Economy Integration

The bio-feedstock industry of China is on the rise against the backdrop of its objectives of carbon neutrality and environmental restructuring. Government initiatives that encourage the production of power using biomass and rural industrialization are increasing the country's agricultural residue take-up and processing capacity.

Widespread interest lies in converting rice husks, corn stover, and food waste into bioethanol, green hydrogen, and biodegradable plastics. Pilot projects for production-scale biomass systems are underway in industrial parks and designated zones across provinces like Shandong and Anhui.

As part of its comprehensive circular economy strategy, China is integrating bio-feedstock development with green financing, emissions trading systems, and waste valorization programs. This coordinated approach positions the country to become a global leader in large-scale biomass utilization, with significant potential for high growth.

Brazil's Strength in Sugarcane-Based Feedstocks and Biochemical Exports

Brazil has become a global example with the oldest program to utilize sugarcane ethanol, in addition to its mature infrastructure for first-generation biofuels. Government incentives, combined mandates, and subsidies for second-generation technologies enhance competitiveness in the bio-based energy and materials industries.

These R&D efforts focus on extracting cellulose from bagasse and forest residues to utilize it in the production of advanced biofuels and bioplastics. This growth is facilitated by partnerships among EMBRAPA, universities and agri-businesses in such states as Minas Gerais and Sao Paulo.

The well-developed export channels and low-carbon production profile enhance Brazil's position in the international biochemical market.

Category-Wise Analysis

Agricultural Residues Power the Transition to Circular Biomass Systems

Wheat straw, corn stover, and rice husks are agricultural wastes that are quickly becoming leaders in sustainable bio-feedstock supply. With large-scale agricultural activities, residues are available in substantial quantities, making the material base economical and environmentally friendly. The fact that they are not considered competitors of traditional food crops makes them a popular target in the 2nd generation biofuel category, aligning well with zero-waste and carbon-neutrality plans advocated by governments and international sustainability commitments.

Agricultural residues are being rapidly integrated into the food industry, with biochemical and thermochemical conversion processes being applied, including fermentation, Hydrolysis, and gasification. Such processes lead to the creation of ethanol, biogas, syngas and advanced biofuels. The versatility of residues across various conversion strategies serves them better in the market, particularly in regions such as India, China, and Brazil, where the amount of agro-wastes is large and energy security is a concern.

Although there are logistics issues surrounding its collection, as well as seasonality and fragmentation in the supply chain, active investments in agri-waste valorization, biomass logistics infrastructure, and feedstock densification technologies are aiding reliable demand. Favorable policies, such as the national bio-energy mission in India and RED II in the EU, are important catalysts.

Biofuels & Renewable Fuels Lead the Decarbonization of Energy Systems

Biofuels & renewable fuels are the biggest and most active sector of the bio-feedstock market. This industry, driven by a global trend toward decarbonizing transportation and power generation, utilizes multiple types of bio-feedstocks, including agricultural wastes, dedicated energy crops, and oleaginous inputs, to produce bioethanol, biodiesel, and sustainable aviation fuels (SAF). The resulting policy pull is due to government requirements, such as the USA Renewable Fuel Standard (RFS) and the EU Renewable Energy Directive (RED II).

The aviation industry, road transport industry, and heavy industries have several applications of biofuels, which serve as a direct channel for reducing fossil fuel reliance. They integrate with the existing fuel infrastructure and increase the use of technological compatibilities (e.g., HEFA, Fischer-Tropsch synthesis) in both developed and emerging economies. Such global leaders in the production of biofuel include the USA, Brazil and Indonesia but new shoots in biofuel production will be experienced in Africa and Southeast Asia.

However, the segment also faces scrutiny related to land use, emissions accounting, and lifecycle efficiency. As a result, innovation in feedstock diversification, advanced conversion pathways, and carbon capture integration is emerging as a pivotal trend shaping the next growth phase of biofuels.

Competitive Analysis

Key players in the bio-feedstock industry include Archer Daniels Midland (ADM), Renewable Energy Group (REG), Suzano, Braskem, Borealis AG, Targray, Sustainable Oils, BioTork, Enerkem, Clariant, Abengoa, INEOS Bio, and Beta Renewables.

There is a high impetus in the bio-feedstock market since industries are transitioning to renewable sources with low-carbon raw materials. Biomass conversion and its applications in fuel, plastics, and specialty chemicals are becoming increasingly efficient. Regulatory policies are driving market adoption of decarbonization, including renewable fuel standards and carbon credits. To enhance sustainability, companies are maximizing the use of high-purity feedstocks, including algae, waste oils, and agricultural waste.

Improving concentration, joint ventures, and internationalization are characteristics of competitive dynamics. Whereas large companies are addressing integrated supply chains and size, start-ups are experimenting with concepts such as waste valorization and carbon-negative manufacturing.

Recent Development

- In May 2025, Braskem celebrated a 37% increase in green ethylene capacity at its Triunfo unit, boosting output to 275,000 tons/year. The expansion supported its I’m green™ polyethylene, sourced from sugarcane ethanol, capturing two tons of CO₂ per ton of ethylene. The move strengthened renewable polymer supply, reinforced farmer partnerships, and advanced sustainability by replacing fossil-based feedstock. The demand for bio-based materials drove growth.

- In May 2025, Borealis unveiled a renewables-based EVA grade for footwear midsoles under its Bornewables™ portfolio. Produced via certified mass balance feedstocks, the material offered virgin-quality performance with lower fossil reliance. Samples of the Cloud 6 midsole debuted at K Show 2025, highlighting Borealis’ push for circular solutions. The launch reinforced collaborations with brands seeking sustainable alternatives for high-performance applications, aligning with industry decarbonization efforts.

Fact.MR has provided detailed information about the price points of key manufacturers of the Bio-Feedstock Market positioned across regions, sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

The 2025 bio-feedstock market report by Fact.MR draws on insights from 4,750 stakeholders spanning 20 countries, with a minimum of 140 respondents per country. Of the participants, 60% were end users-including automotive OEMs, architectural glazing contractors, electronics manufacturers, and photovoltaic panel assemblers-while the remaining 40% comprised adhesive formulators, material scientists, procurement leads, and regulatory compliance experts.

Data collection occurred between June 2024 and May 2025, with a targeted focus on key variables such as performance under high-stress conditions, cross-substrate adhesion reliability, curing efficiency, sustainability parameters, and alignment with evolving VOC and chemical safety guidelines. A calibrated regional balancing model was applied to ensure proportional representation across all major markets.

The research reviewed over 150 validated sources, including technical literature, patent disclosures, ISO certifications, SDS documents, and financial disclosures from leading manufacturers to triangulate and refine findings.

Fact.MR applied rigorous analytical tools such as multi-variable regression and scenario modeling to ensure data robustness. With continuous monitoring of the glass adhesives space since 2018, this report offers a comprehensive roadmap for companies seeking competitive advantage, innovation, and sustainable growth within the sector.

Segmentation of Bio-Feedstock Market

-

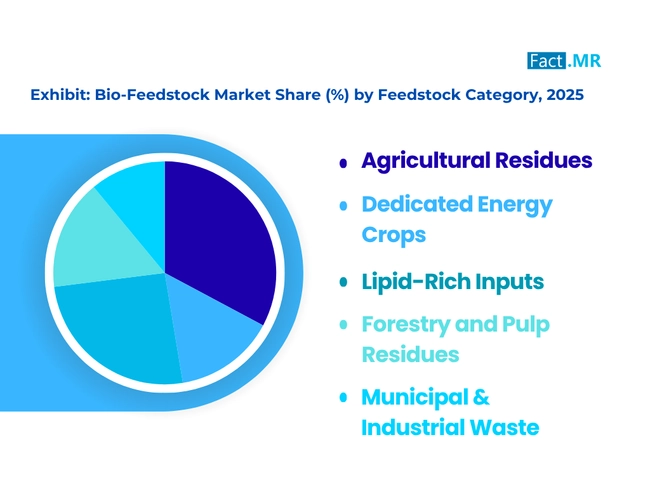

By Feedstock Category :

- Agricultural Residues

- Dedicated Energy Crops

- Lipid-Rich Inputs

- Forestry and Pulp Residues

- Municipal & Industrial Waste

-

By Conversion Pathway Compatibility :

- Biochemical (Fermentation, Hydrolysis)

- Lipid-based (Transesterification, HEFA)

- Thermochemical (Pyrolysis, Gasification)

- Anaerobic Digestion (AD)

- Hybrid / Emerging (HTL, Catalysis)

-

By Sustainability Tier :

- 1st Generation

- Corn

- Sugarcane

- Vegetable Oils

- 2nd Generation

- Agri Residues

- Wood Waste

- Bagasse

- 3rd Generation

- Algae

- Seaweed

- Photosynthetic Biomass

- Waste-Based & Recycled

- MSW

- UCO

- Sludge

- 1st Generation

-

By Application Industry :

- Biofuels & Renewable Fuels

- Bio-Chemicals

- Bio-Plastics & Packaging

- Power & Heat Generation

- Animal Feed & Nutraceuticals

- Carbon Products

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Bio-Feedstock Market Size Reported by Fact.MR for 2025?

The global bio-feedstock market was valued at USD 122.1 billion in 2025.

Who are the Major Players Operating in the Bio-Feedstock Market?

Prominent players in the market are Archer Daniels Midland (ADM), Renewable Energy Group (REG), Suzano, Braskem, among others.

What is the Estimated Valuation of the Bio-Feedstock Market in 2035?

The market is expected to reach a valuation of USD 224.9 billion in 2035.

What Value CAGR did the Bio-Feedstock Market Exhibit Over the Last Five Years?

The historic growth rate of the bio-feedstock market was 5.8% from 2020 to 2024.