Ethylene Vinyl Acetate Market Outlook (2025 to 2035)

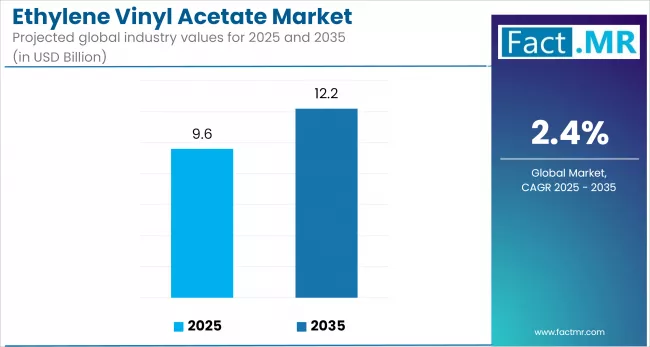

The global ethylene vinyl acetate market is projected to increase from USD 9.6 billion in 2025 to USD 12.2 billion by 2035, with an annual growth rate of 2.4%, driven by rising demand in the footwear, solar energy, flexible packaging, and wire & cable insulation sectors.

Ethylene vinyl acetate’s role in solar encapsulants, lightweight footwear components, and flexible films supports its use across diverse sectors. Innovation in bio-based and recyclable ethylene vinyl acetate is expected to generate additional opportunities, particularly in regions prioritizing material circularity and waste reduction.

What are the Drivers of the Ethylene Vinyl Acetate Market?

The growth of the ethylene vinyl acetate market is being driven by rising demand across several high-impact industries. In footwear manufacturing, ethylene vinyl acetate is widely used in midsoles and insoles due to its lightweight and cushioning properties, which support large-scale production in key markets such as China, Vietnam, and India.

The rapid expansion of solar energy is another major factor, as ethylene vinyl acetate serves as a key encapsulant in photovoltaic (PV) modules. With global solar installations exceeding 400 GW in 2023, ethylene vinyl acetate consumption in this segment continues to rise.

The packaging industry is also adopting ethylene vinyl acetate for its flexibility, seal strength, and compatibility with multilayer films, especially in food, healthcare, and e-commerce applications. In the electrical infrastructure sector, ethylene vinyl acetate is being increasingly used in wire and cable insulation, driven by growing investments in power grids and renewable energy.

Its biocompatibility further supports applications in medical tubing and devices, aligning with the rising demand for healthcare. Regulatory and environmental pressures are encouraging its use as a low-VOC, non-toxic alternative to conventional plastics, with increasing interest in bio-based and recyclable formulations driving innovation across the value chain.

What are the Regional Trends of the Ethylene Vinyl Acetate Market?

The ethylene vinyl acetate market exhibits strong regional variation shaped by industrial priorities, regulatory frameworks, and end-user demand. The Asia-Pacific region dominates global ethylene vinyl acetate (EVA) consumption, led by China, which benefits from its integrated manufacturing capabilities and large-scale production in the footwear, solar encapsulants, and packaging materials sectors. India is also emerging as a key market, driven by government-backed solar expansion and the "Make in India" initiative in the electronics and automotive sectors.

North America exhibits steady growth, driven by increasing investments in renewable energy infrastructure, flexible packaging, and wire and cable insulation, particularly in the USA, where clean energy policies are stimulating demand for solar and grid modernization.

In Europe, stricter regulations on emissions and recyclability are pushing demand for sustainable ethylene vinyl acetate formulations, especially in automotive interiors, consumer packaging, and medical applications. Countries like Germany and France are leading the way in innovation for bio-based alternatives.

Meanwhile, Latin America is witnessing moderate growth, led by Brazil and Mexico, where usage is concentrated in footwear manufacturing and basic packaging. The Middle East and Africa, although still developing, are seeing a rising demand for construction, cables, and industrial films, supported by infrastructure initiatives in the UAE, Saudi Arabia, and South Africa.

What are the Challenges and Restraining Factors of the Ethylene Vinyl Acetate Market?

The ethylene vinyl acetate market faces several structural and operational challenges that may constrain long-term growth. A key concern is the volatility of raw material prices, particularly for ethylene and vinyl acetate monomer (VAM), both of which are derived from petroleum-based feedstocks. Fluctuations in crude oil prices and global supply chain disruptions triggered by geopolitical tensions or logistics bottlenecks can significantly impact production costs and manufacturers' margins.

Environmental regulations are also tightening, especially in Europe and North America, where concerns over VOC emissions, non-recyclability, and the lifecycle impacts of conventional grades are drawing increased scrutiny from regulators and end-users.

Recyclability remains a constraint, particularly in multilayer films and solar encapsulants, where technical and economic barriers to separation limit circularity and create compliance risks amid growing sustainability mandates. Ethylene vinyl acetate also competes with alternatives such as thermoplastic polyurethanes (TPU), polyolefin elastomers (POE), and bio-based polymers that offer comparable performance with improved environmental profiles in select applications.

Technical limitations are evident in high-temperature and structural applications, where their thermal resistance and mechanical strength underperform compared to advanced engineering plastics. The slower adoption of bio-based ethylene vinyl acetate due to high costs, limited availability, and underdeveloped infrastructure further restricts large-scale shifts toward sustainable formulations.

Country-Wise Outlook

Steady Growth in the USA Ethylene Vinyl Acetate Market Driven by Packaging, Solar, and Industrial Demand

The U.S. ethylene vinyl acetate (EVA) market is experiencing consistent growth, driven by rising demand across various applications, including packaging, renewable energy, footwear, and industrial uses. In packaging, ethylene vinyl acetate is widely used in hot-melt adhesives and multilayer film structures due to its strong sealing properties, flexibility, and compatibility with food-grade applications. The continued expansion of e-commerce and rising demand for lightweight, durable packaging materials are driving the consumption of ethylene vinyl acetate across supply chains.

The solar energy sector has emerged as a key growth driver, with ethylene vinyl acetate serving as a critical encapsulant in photovoltaic (PV) modules. Federal incentives and state-level clean energy mandates are accelerating the deployment of solar systems, thereby increasing demand for durable, high-performance materials such as ethylene vinyl acetate. In footwear manufacturing, it remains a preferred material for midsoles and cushioning due to its resilience and comfort, supporting sustained demand from both domestic and global brands operating in the USA.

Its role in wire and cable insulation is also expanding with the growth of grid modernization, electric vehicle infrastructure, and broader electrification trends. However, the market faces pressure from sustainability initiatives, as manufacturers pursue recyclable and bio-based alternatives with comparable performance. Despite these challenges, innovation in material formulations and processing is helping position ethylene vinyl acetate as a versatile solution across multiple high-growth sectors.

China’s Ethylene Vinyl Acetate Market Sustains Momentum Amid Industrial Modernization and Renewable Energy Push

China continues to lead the global ethylene vinyl acetate market, supported by its expansive industrial base, integrated raw material supply chains, and strong downstream demand across key sectors. Ethylene-vinyl acetate (EVA) consumption in China is particularly robust in the footwear manufacturing sector, where the country dominates global production, supplying a significant share of midsole components for both domestic and export markets.

China's rapid expansion in solar energy is also driving increased demand for ethylene vinyl acetate. The material is essential for encapsulating photovoltaic (PV) cells, and with the nation accounting for more than one-third of global solar installations, demand remains strong. In 2023 alone, China added over 216 GW of new solar capacity, significantly outpacing other regions. Local manufacturers, such as Levima Advanced Materials and Sinopec, have expanded production to meet the rising demand from module producers like LONGi and JinkoSolar.

Beyond renewables and footwear, ethylene vinyl acetate is increasingly used in packaging films, automotive interiors, hot-melt adhesives, and wire and cable insulation. Domestic consumption is rising with e-commerce growth, EV adoption, and infrastructure investment. China's industrial upgrading, driven by smart manufacturing and automation, is also increasing demand for high-performance ethylene vinyl acetate grades with improved thermal stability and enhanced processing efficiency.

While China benefits from scale and cost competitiveness, the market is under growing pressure to adopt environmentally sustainable practices. Regulatory frameworks around emissions, recycling, and material safety are tightening, prompting innovation in recyclable and bio-based ethylene vinyl acetate formulations.

Japan Sees Steady Growth in Ethylene Vinyl Acetate Driven by Solar, Adhesives, and Advanced Materials

Japan’s ethylene vinyl acetate market continues to advance, supported by the country’s focus on clean energy, high-performance manufacturing, and material innovation. Demand from the solar photovoltaic sector remains strong, with ethylene vinyl acetate serving as a key encapsulant in solar panels, valued for its durability, UV resistance, and optical clarity. National initiatives to expand solar infrastructure have reinforced this trend.

Ethylene vinyl acetate is also increasingly used in hot-melt adhesives, packaging films, and automotive interiors due to its flexibility, bonding strength, and ease of processing. Japanese manufacturers are developing specialized grades for medical devices, semiconductor packaging, and flexible electronics, where material purity and reliability are critical.

With a strong industrial base and a long-standing emphasis on precision engineering, Japan is positioning ethylene vinyl acetate as more than a commodity polymer. It is being applied as a strategic material in advanced, high-value sectors. The market benefits from continuous innovation, regulatory alignment, and the nation’s commitment to efficient and sustainable material solutions.

Category-wise Analysis

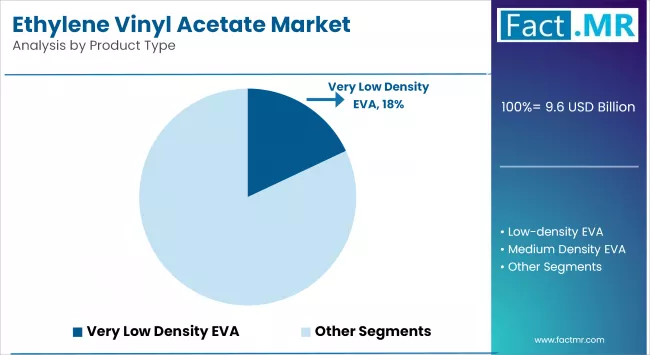

Low-density ethylene vinyl acetate to Exhibit Leading Share Among Product Type

Low-density ethylene vinyl acetate (LD-ethylene vinyl acetate) continues to hold the largest share within the ethylene vinyl acetate product segment due to its cost-efficiency, wide applicability, and ease of processing. It is used extensively in packaging films, hot-melt adhesives, foam products, and wire and cable insulation, offering flexibility and optical clarity in end-use applications.

In footwear production, LD-ethylene vinyl acetate remains the dominant choice for midsoles and outsoles, valued for its lightweight and cushioning capabilities. Packaging manufacturers utilize it in multilayer structures and sealing layers, especially in food and pharmaceutical films, where softness and seal integrity are essential.

Its compatibility with extrusion and injection molding processes enables scalable, high-throughput production. As global demand rises for materials that balance durability and performance at low cost, LD-ethylene vinyl acetate is expected to retain its position across both traditional and emerging sectors, including solar encapsulation, automotive interiors, and healthcare components.

Ongoing investments in processing technology and vertical integration, particularly in the Asia-Pacific and North America regions, have reinforced the commercial viability of LD-ethylene vinyl acetate as the most widely adopted grade in the global ethylene vinyl acetate market.

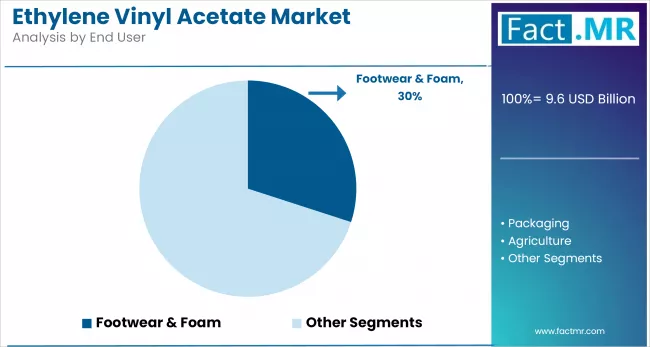

Footwear & Foam Category to Hold Leading Share in Ethylene Vinyl Acetate Market

The footwear and foam segment continues to account for the highest consumption of ethylene vinyl acetate, driven by the material’s lightweight construction, flexibility, and shock-absorbing characteristics. Ethylene vinyl acetate is widely used in midsole and outsole components across athletic, casual, and occupational footwear, particularly in large-scale manufacturing hubs such as China, Vietnam, and India. Its cost-efficiency and ease of processing make it a material of choice for global footwear producers.

In non-footwear applications, ethylene vinyl acetate (EVA) foams are utilized in sports equipment, yoga mats, automotive interiors, protective padding, and general consumer products due to their resilience and rapid compression recovery. Processing compatibility with injection and compression molding supports efficient volume production across these uses.

Ongoing demand for ergonomic, comfortable footwear and increased interest in lightweight, low-emission materials continue to support segment growth. Product development in bio-based ethylene vinyl acetate foam and advanced polymer blends is also expanding usage in premium footwear, orthotic devices, and medical cushioning products.

With sustained demand from both developed and developing economies, the footwear and foam segment is projected to retain its dominant position in the ethylene vinyl acetate value chain over the forecast period.

Asia Pacific Holds Leading Share in Ethylene Vinyl Acetate Market

The Asia Pacific region maintains its dominant position in the global ethylene vinyl acetate market, supported by expansive manufacturing capacity, cost-effective production, and consistent demand across key end-use sectors. China remains the primary driver, enabled by its vertically integrated supply chain, extensive solar module production, and leadership in footwear and flexible packaging exports. Accelerated investment in solar photovoltaic deployment has further solidified China’s role as a major consumer of ethylene vinyl acetate in encapsulation systems.

India is registering rapid growth, underpinned by infrastructure expansion, policy-led industrialization, and increasing domestic demand for ethylene vinyl acetate-based films, footwear materials, and adhesives. South Korea and Japan contribute through high-value applications in electronics, precision packaging, and automotive interiors.

The region's competitive advantage is reinforced by its export-oriented output, which serves Europe, North America, and the Middle East. With active capacity expansion, favorable policy frameworks, and growing interest in advanced polymer materials, Asia Pacific is expected to retain its leading share in the ethylene vinyl acetate market through the forecast period.

Competitive Analysis

The ethylene vinyl acetate market is characterized by a diverse and competitive landscape, comprising established global petrochemical firms and regional producers focused on material innovation, cost leadership, and downstream integration. Leading players, such as Arkema Group, ExxonMobil Corporation, Dow Chemical Company, Braskem S.A., and Celanese Corporation, maintain strong positions through their large-scale production capacity, proprietary process technologies, and extensive supply networks.

Companies like ARLANXEO Holding B.V., LyondellBasell Industries N.V., and Clariant AG specialize in specialty formulations and value-added applications, including ethylene vinyl acetate variants for medical devices, high-performance films, and automotive components. Meanwhile, regional producers such as Asia Polymer Corporation, Formosa Plastics Corporation, Hanwha Total Petrochemical, and Sahara International Petrochemical Company (SIPCHEM) are expanding capacity across Asia and the Middle East to meet rising demand in packaging, footwear, solar energy, and adhesives.

The competitive environment is further shaped by strategic partnerships, feedstock integration, and investments in bio-based ethylene vinyl acetate and low-VOC formulations, particularly in response to regulatory pressures and customer sustainability goals. As product differentiation gains importance, market players are emphasizing supply chain agility, application-specific research and development, and expansion into high-growth regions to maintain and grow their market share.

Recent Development

- In September 2024, Dow-Mitsui Polychemicals launched ISCC-certified biomass-based ethylene vinyl acetate (EVA FLEX) and LDPE, enabling the direct replacement of petroleum-based versions while reducing lifecycle greenhouse gas emissions.

- In 2023, LyondellBasell and PetroChina Guangxi licensed high-pressure Lupotech T technology for new LDPE/ethylene vinyl acetate lines.

Segmentation of Ethylene Vinyl Acetate Market

-

By Product Type :

- Very Low Density ethylene vinyl acetate

- Low-density ethylene vinyl acetate

- Medium Density ethylene vinyl acetate

- High-density ethylene vinyl acetate

-

By End User :

- Footwear & Foam

- Packaging

- Agriculture

- Photovoltaic Panels

- Pharmaceuticals

- Other End-use Industries

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South Asia

- Oceania

- MEA

- Frequently Asked Questions -

What is the Global Ethylene Vinyl Acetate Market Size in 2025?

The ethylene vinyl acetate market is valued at USD 9.6 billion in 2025.

Who are the Major Players Operating in the Ethylene Vinyl Acetate Market?

Prominent players include Dow Chemical Company, ExxonMobil Corporation, Formosa Plastics Corporation, Hanwha Solution Chemical Division Corporation, and others.

What is the Estimated Valuation of the Ethylene Vinyl Acetate Market by 2035?

The market is expected to reach a valuation of USD 12.2 billion by 2035.

What Value CAGR Did the Ethylene Vinyl Acetate Market Exhibit over the Last Five Years?

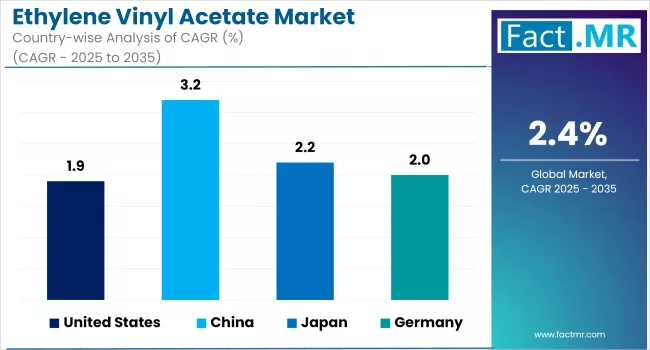

The historic growth rate of the ethylene vinyl acetate market was 1.9% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed