Triazole Market Outlook (2025 to 2035)

The triazole market will be valued at USD 810.1 million by 2025 end, as per Fact.MR analysis, the industry will grow at a CAGR of 4.5% and reach USD 1,251.9 million by 2035.

In 2024, the global industry for triazoles saw moderate but focused growth, with major developments led by individual end-use industries as opposed to across-the-board demand. In the agrochemical industry, fungicides enjoyed growing acceptance in South American countries as a result of unusual crop diseases and increased agricultural exports. The pharmaceutical sector also saw greater usage of product intermediates, especially antifungal APIs, driven by increasing cases of systemic fungal diseases among aging populations in North America and certain parts of Europe.

At the same time, realignments of supply chains influenced pricing and delivery schedules, most notably for those intermediates derived from Asia. Raw material prices for 1,2,4-triazole compounds also saw volatility in the wake of petrochemical price fluctuations early in 2024.

Looking ahead to 2025 and beyond, the industry will continue its growth trend, driven mainly by regulatory clearances for new triazole-based crop protection chemicals and the increasing significance of specialty triazoles in materials science and biopharmaceutical R&D. Developments on green synthesis routes and low-toxicity formulations will also shape product development cycles. East Asia will likely be the most profitable regional hub, with demand and production capacities growing through 2035.

Key Metrics

| Metrics | Values |

|---|---|

| Industry Size (2025E) | USD 810.1 million |

| Industry Value (2035F) | USD 1,251.9 million |

| Value-based CAGR (2025 to 2035) | 4.5% |

Fact.MR Survey on Triazole Industry

Fact.MR Stakeholder Survey Data: Trends on the Basis of Stakeholder Opinion

(Surveyed Q4 2024, n=520 stake participant groups, including agrochemical companies, pharmaceuticals manufacturers, chemical suppliers, and regulatory experts within the US, Western Europe, China, India, and Japan)

Stakeholder Priority Areas

- Compliance with regulations: 79% of all stakeholders worldwide termed compliance with REACH, EPA, and local pesticide/medicine regulations as a "high priority."

- Stability in formulation: 71% prioritized triazole-based substances' shelf-stability, particularly in high-humidity industries.

- Multi-functionality: 68% wanted broader-spectrum activity in agrochemical use to reduce product layering.

Regional Variance:

- US: 64% emphasized the need for dual-use (fungicidal + growth regulation), compared with 33% in Japan.

- Europe: 82% requested low-residue formulations to suit the EU's Farm to Fork policy, compared with 46% in India.

- China/India: 59% preferred economical formulations for volume-based cover crop management, compared with 28% in Western Europe.

Adoption of Advanced Synthesis and Delivery Technologies

Innovation Embrace:

- US: 53% of respondents reported shifting to nano-emulsified triazoles for enhanced bioavailability in pharma.

- Western Europe: 61% utilized slow-release or encapsulated triazoles in sustainable farming trials (notably in Germany and the Netherlands).

- Japan: Only 25% had adopted advanced formulations, citing legacy equipment compatibility and small-batch processing.

- India/China: 42% applied microencapsulation tech in agrochemicals to minimize environmental run-off.

ROI Perspectives:

- US: 69% said premium product solutions are “worth the investment” in high-margin pharma/agriculture applications.

- India: 58% chose low-cost input options over innovation because of price-conscious rural end-users.

Preference in Materials and Inputs

Input Base:

- 1,2,4-Triazole: Most preferred by 66% of the respondents due to its flexibility in both pharma and crop protection.

- 1,2,3-Triazole: Selected by 34%, predominantly pharma-oriented manufacturers for synthetic APIs.

Regional Trends:

- Western Europe: 54% concentrated on "green chemistry" processes for product synthesis (e.g., solvent-free, enzymatic).

- China/India: 62% continued using traditional chemical routes because of low infrastructure cost.

- US: 46% moving towards solvent recovery technologies in the production of triazoles.

Price Sensitivity and Procurement Issues

Global Pressures:

- 84% mentioned raw material price volatility, particularly from petrochemical feedstock prices and Chinese export controls.

Regional Preferences:

- Western Europe/US: 57% would pay a premium of 10–15% for high-purity, pharma-grade triazoles.

- India/Japan: 74% requested bulk packaging discounts and cost-effective intermediates.

- Japan: 48% showed a preference for domestic procurement owing to high import taxes.

Pain Points in the Value Chain

Manufacturers:

- US: 58% reported difficulty of scaling pilot-stage green synthesis to commercial production volumes.

- Europe: 52% mentioned compliance hurdles with REACH documentation for newer derivatives.

- India/China: 63% wrestled with inconsistent QA/QC by third-party contract manufacturers.

Distributors:

- Europe: 49% mentioned slower-than-projected industry penetration for newer triazoles because of re-approvals at the regulatory level.

- India: 55% experienced logistics breakdowns during monsoons, impacting agrochemical supplies.

- End-Users (Pharma/Agrochemical Companies):

- US: 44% mentioned escalating costs of purification as a major obstacle.

- China: 61% mentioned inconsistency of quality in imported product intermediates.

- Japan: 37% grappled with unavailable tech support to incorporate new triazoles in old production setups.

Future Investment Priorities

Consensus:

- 73% of international stakeholders intend R&D investment into green and high-yield synthesis techniques.

Regional Focus:

- US: 59% investing in dual-use derivatives for agri and pharma applications.

- Europe: 64% investing in residue-free formulation with respect to stringent food safety regulations.

- India/China: 52% investing in cost-reduced scale-up synthesis for export.

Regulatory Impact:

- US: 67% referred to EPA's new fungicide evaluation guidelines as creating formulation delays and batch reformulations.

- Western Europe: 78% considered EU pesticide and pharmaceutical directives as drivers of high-purity product demand.

- China/India: Only 39% viewed major regulatory impact, citing low enforcement pressure and less stringent approval routes.

- Japan: 44% indicated that continuous chemical reclassification regulations postponed uptake of specific product variants.

Conclusion: Variance vs. Consensus

High Consensus:

- Demand for triazole-based compounds is rising in both the agrochemical and pharmaceutical industries.

- Stakeholders universally concur on the significance of purity, stability, and cost control.

A. Key Variances:

- US/Europe: Innovation-first and regulatory convergence priorities.

- India/China: Volume-first approaches with incremental innovation take-up.

- Japan: Conservative technology adoption and high cost and system compatibility focus.

Strategic Insight:

- Customized industry strategies are critical; US/EU formulation innovation, cost leadership in Asia, and low-residue, compact products for Japan will drive industry success up to 2035.

Government Regulations on Triazole Industry

| Country | Regulatory Environment & Mandatory Certifications |

|---|---|

| U.S. | EPA (Environmental Protection Agency) requires product fungicides to meet stringent toxicity and residue tolerance levels under FIFRA (Federal Insecticide, Fungicide, and Rodenticide Act). Mandatory EPA registration for all triazole-based agrochemicals. (Source: EPA) |

| Canada | They are used and governed by PMRA (Pest Management Regulatory Agency) under Health Canada. Requires comprehensive environmental risk assessments. Products must have PMRA registration and MRL (Maximum Residue Limits) compliance. |

| Germany | Highly regulated under REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals). Triazole-based fungicides must be EU-registered and classified with CLP labeling. BfR (Federal Institute for Risk Assessment) oversees health risk data. |

| France | EU REACH compliance is mandatory. Agriculture is regulated under ANSES the French Agency for Food, Environmental and Occupational Health & Safety). Substances must undergo ecotoxicological testing for field application approval. |

| Italy | Regulated by the Ministry of Health and EFSA in coordination with EU REACH. Mandatory labeling as per EU’s CLP regulations for toxicity. Ongoing scrutiny on endocrine-disrupting properties of certain compounds. |

| UK | Post-Brexit, now follows UK REACH, largely aligned with EU REACH but with its own Health and Safety Executive (HSE) evaluations. All products fungicides require UK-specific registration. Tight controls on residues in cereals and fruits. |

| Japan | Regulated under CSCL (Chemical Substances Control Law) and Agrochemicals Regulation Law. All fungicides require approval from the Ministry of Agriculture, Forestry and Fisheries (MAFF). High scrutiny on persistence in soil and groundwater. |

| South Korea | Governed by K-REACH and Agrochemicals Control Act. Requires full toxicological data submission and environmental risk assessment. Agro-triazoles must also meet RDA (Rural Development Administration) guidelines. |

| China | Regulated under MEE (Ministry of Ecology and Environment) and ICAMA (Institute for the Control of Agrochemicals, Ministry of Agriculture). Requires New Chemical Substance Notification (NCSN) under MEP Order No. 7. Mandatory product registration. |

| India | Governed by the Insecticides Act (1968) and monitored by Central Insecticides Board and Registration Committee (CIBRC). All triazoles require mandatory registration with CIBRC. Growing focus on green chemistry alternatives to synthetic triazoles. |

Market Analysis

The industry for triazoles is set to grow steadily over the next decade to 2035, led by mounting demand for potent and broad-spectrum fungicides in agriculture and turf management. Enhanced regulatory attention and sustainability demands are driving manufacturers toward safer, low-residue products to the advantage of innovation-driven players. Legacy chemists or companies with limited compliance strength might, however, face challenges in staying competitive in regulated environments.

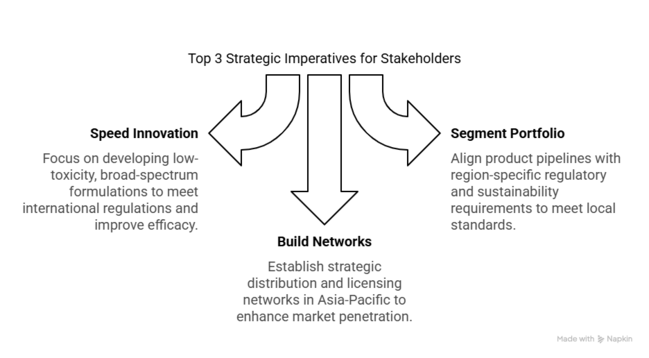

Top 3 Strategic Imperatives for Stakeholders

Speed Innovation in Low-Toxicity, Broad-Spectrum Formulations

Managers should invest in R&D of next-generation triazoles that conform to new, internationally changing regulatory levels (e.g., EU REACH, US EPA) while offering improved efficacy on a broad range of crops and temperatures. R&D partnerships should be prioritized for bio-based synergists and resistance-management technologies.

Segment Portfolio by Region-Specific Regulatory and Sustainability Requirements

Realign product pipelines to align with country-level compliance standards like zero-residue regulations in Western Europe or safe-handling standards in Japan. Highlight certifications (e.g., GHS, EU Biocidal Product Regulation) and eco-labels that appeal to end-users and regulators.

Build Strategic Distribution and Licensing Networks in Asia-Pacific

With the highest CAGR (5.1%) in East Asia, form localized distribution partnerships and enter into licensing arrangements with local agrochemical companies. This will hasten industry penetration while reducing regulatory setbacks and logistics risks.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability/Impact |

|---|---|

| Regulatory Bans on Specific Compounds in the EU and Japan | High |

| Rising Resistance of Fungal Pathogens to Existing product Formulations | Medium |

| Raw Material Price Volatility Due to Supply Chain Disruptions | High |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Evaluate Regulatory Exposure in Key players | Conduct feasibility studies on reformulating or substituting restricted triazoles (e.g., tebuconazole, propiconazole) in the EU and Japan |

| Strengthen Product Pipeline Against Resistance | Initiate R&D collaborations to develop combination fungicides or multi-site action molecules. |

| Mitigate Raw Material Price Risk | Secure forward contracts or explore local sourcing options for product intermediates in India and Southeast Asia. |

For the Boardroom

To stay ahead in the industry, the client must pivot from a volume-first strategy to a resilience- and compliance-led roadmap. With tightening regulations across the EU and Japan, coupled with rising resistance in staple crops like wheat and soy, the company should immediately prioritize next-gen product development, focusing on lower-residue, resistance-managed formulations.

Strategic investment in dual-mode fungicides and sustainable agri-solutions (e.g., triazole-biological hybrids) will unlock high-value partnerships in Latin America and Southeast Asia, where adoption barriers are lower. This intelligence signals a shift: Winning in 2025 and beyond means aligning R&D, supply chain security, and policy foresight, not just share.

Segment-wise Analysis

By Form

The liquid segment is expected to register an 6% share, the highest under the form category in 2025. The liquid state finds extensive application owing to its enhanced ease of use and versatility across various industries, especially in pharmaceuticals and agriculture. In agriculture, the liquid form enables accurate, uniform spraying that is critical in large-scale crop protection, facilitating effective coverage and improved plant absorption.

Liquid triazoles are also preferred due to their ease of dissolving in solvents, which makes them more effective in a range of formulations such as emulsions or concentrates. In pharmaceutical applications, liquid triazoles are used for injectable medications and topical applications because they can easily be administered and absorbed.

By Grade

The >98% grade is commonly used because it is of extremely high purity, which is necessary for applications where precision and reliability are needed, especially in the pharmaceutical and research industries. It will grow at a CAGR of 5%, the most profitable section during the forecast period. These compounds of higher purity are of vital importance to R&D laboratories where accuracy and consistent results are of utmost importance.

In drug making,>98% purity is desired due to its capability to guarantee stability and efficacy in drug preparations, especially for crucial treatments like antifungals or anticancer medications. >98% grade triazole, with its low molecular weight and high boiling point, is suited for use in sensitive formulations with improved control of reactions and improved effectiveness in the delivery of active ingredients.

By End Use

The pharmaceutical segment will be most profitable with a CAGR of 4.9% in 2025. The pharmaceutical industry extensively employs product because of its pivotal position in the synthesis of antifungal and anticancer medications. Triazoles, as a group of compounds, are extremely useful in the treatment of fungal infections, which are becoming more common, especially among immunocompromised individuals.

Their mechanism of inhibiting fungal growth by interfering with cell membrane synthesis makes them invaluable in medical therapies for diseases such as athlete's foot, ringworm, and systemic infections. Moreover, the increase in chronic diseases like cancer and diabetes has fueled the need for derivatives, which are utilized in the synthesis of therapeutic agents. Triazoles are also utilized in the treatment of tuberculosis and other infectious diseases, further increasing their demand in the pharmaceutical sector.

Country-wise Analysis

U.S.

The industry in the U.S. is anticipated to grow at a CAGR of 5.0% during the forecast period.It is mainly supported by the extensive demand from both the pharmaceutical and agricultural industries. The pharma industry, especially, is growing thanks to the growth in the incidences of long-term diseases such as cancer, diabetes, and fungal diseases, which need antifungal drugs wherein product forms the central constituent.

The agrochemicals sector in America is also seeing consistent growth where product constitutes a major additive in pesticides where its use specifically protects crops, especially in monoculture farming practices. The focus on compliance with regulations and product formulation innovation will also stimulate growth. The U.S. is also a pioneer in agricultural technology, and this practice is likely to continue, pushing the use of products in agrochemicals.

UK

Uk’s sales is predicted to witness a CAGR of 4.3% during the forecast period. The pharmaceutical industry is one of the main drivers of such growth, particularly with the growing prevalence of fungal infections and cancer, which call for treatments such as antifungal product medicines. The UK also enjoys a mature pharmaceutical R&D system, which is driving innovation in drug development.

The agricultural sector's growth, although slower than in other regions, is also driving demand for triazoles, especially in crop protection products. Ecological issues have been the driving force behind a transition to eco-friendly agricultural methods, and triazole-based pesticides remain an assured remedy. The UK's regulatory system aids the development of the pharma and agrochemical industries, with strict drug development and agricultural product formulation regulations guaranteeing quality standards.

France

The industry in France is anticipated to expand with a CAGR of 4.5% from 2025 to 2035. The industry is boosted by robust demand from the pharmaceutical industry, as triazoles are extensively employed in pharmaceuticals for antifungal medications and cancer.

France's strong healthcare system, combined with its emphasis on medical research and drug development, continues to drive an expanding pharmaceutical sector. The mounting occurrence of chronic conditions such as fungal infections and cancer, is likely to propel demand for derivatives.

Additionally, the French agricultural sector continues to be a major consumer of product as an ingredient in pesticides, which aids in crop protection against fungal diseases.

Italy

The industry in Italy is expected to grow at a CAGR of 4.1% from 2025 to 2035. Italy's pharma industry remains on the upswing because the demand for therapy for fungal infection and cancer continues to grow, in which case triazoles are critical components.

The established pharma industry in Italy and the focus it has on R&D support stable demand for products with high purity, especially for formulations used in drugs. The farming industry in Italy also contributes greatly to the industry, with triazoles being extensively applied to pesticides to safeguard crops from fungal infections.

Italian agriculture is centered on sustainability as well as high-quality production, with pressure on regulations to employ more environmentally friendly solutions. As the nation continues to invest in its agricultural and pharmaceutical industries, demand for product is anticipated to experience steady growth, especially in pharmaceutical uses for the management of chronic diseases and in agriculture for crop protection.

South Korea

The landscape in South Korea is expected to grow at a CAGR of 5.2% from 2025 to 2035. This is due to South Korea's well-developed pharmaceutical sector, which is investing heavily in the development of antifungal drugs, and the rising cases of fungal infections and cancer. The compounds, especially for use in medicine, are essential to the nation's treatment.

The agricultural industry of South Korea is also responsible for creating demand for triazole-derived pesticides, and crop protection as well as green farming is given importance. Increased usage of triazoles in agrochemicals is supported by the increased trend of precision agriculture and environmental sustainability in the country. With the expansion of the healthcare industry and advancing agricultural technologies, South Korea will remain an important contributor to the industry in the next few years.

Japan

Japan’s sales is expected to register a CAGR of 4.0% from 2025 to 2035. The pharmaceutical industry in Japan remains one of the largest in the world, with a focus on developing innovative treatments for chronic diseases, including cancer and fungal infections. This will continue to drive the demand for product in the pharmaceutical sector. Still, the growth in Japan's agricultural sector is comparatively slower because of land limitations, which restrict the overall demand for agrochemicals such as triazole.

Moreover, Japan's emphasis on precision farming and sustainable agriculture will continue to foster the use of product in pesticide formulations. Although the nation is not likely to experience similar high-speed growth as other nations, Japan's well-established pharmaceutical infrastructure will see a steady, but slower, demand for triazole.

China

The industry in China is expected to grow at a CAGR of 5.4% during the forecast period, due to both the pharmaceutical and agricultural industries. Being one of the world's largest pharma industries, China's expanding healthcare sector is experiencing higher demand for product in antifungal therapies and cancer drug development. The increased incidence of chronic diseases in China also supports the growth of the industry.

Further, China's largest agricultural sector relies heavily on pesticides such as triazole to treat fungal diseases in crops. With more government spending in pharmaceutical and agricultural industries, the industry is anticipated to grow significantly in China during the forecast period.

Competitive Landscape

Major players in the triazole industry are concentrating on innovation, strategic alliances, and geographical expansion to consolidate their market positions. They are undertaking research and development to develop more efficient and eco-friendly triazole-based products. Strategic alliances with local distributors and agricultural associations are assisting these firms to increase their presence in developing markets.

As far as pricing is concerned, businesses are implementing competitive pricing strategies to win cost-conscious customers, particularly in emerging markets. They are also seeking opportunities to streamline their supply chains to lower production costs and increase profit margins.

Key trends in 2024 are heightened mergers and acquisitions to strengthen market positions and broaden product offerings. Companies are also prioritizing sustainable operations, conforming to international environmental policies and consumers' demands for environmentally friendly products.

In general, the triazole market is undergoing dynamic transformation, with firms aggressively seeking strategies to improve competitiveness and address the changing needs of the agricultural industry.

Market Share Analysis

Adama Agricultural Solutions Ltd.: (15-20%)

Adama is among the largest companies in the industry, particularly in agrochemical uses. Adama has a diversified range of products that address different agricultural requirements, where triazole features prominently in their crop protection offerings.

Adama's established industry presence is underpinned by its large distribution network in several regions, such as North America, Europe, and Asia-Pacific. The firm specializes in offering affordable yet highly effective formulations that translate into maximum pest and disease control, thus cementing its place in the industry.

UPL Limited: (12-18%)

UPL Limited is a major dominant force in the agrochemical as well as pharmaceutical segments of the industry. UPL has built a strong presence in geographies like Latin America, Asia-Pacific, and North America, where its robust distribution network is the key to its leadership.

UPL's focus on sustainability, research and development, and product innovation enables it to stay competitive in the shifting industry. The diversified portfolio of the company, encompassing crop protection as well as pharmaceutical-grade products, enables it to cover many applications, further broadening its reach.

Arysta LifeScience Corporation: (10-15%)

Arysta LifeScience boasts a significant position in the agrochemical industry, especially crop protection via derivatives. With its array of diverse agrochemical offerings, the firm is a primary driver in assisting farmers in pest and disease management.

UPL Limited's acquisition of Arysta further consolidated its industry strength and added to UPL's leadership in the segment. This acquisition afforded UPL better access to novel products and an expanded distribution platform, making Arysta an integral component of UPL's global growth model.

Cheminova A/S (Owned by FMC Corporation): (8-12%)

The FMC-owned Cheminova, formerly independent, has long had a stable share in the global industry, particularly in fungicide and pest control product ranges. The history of the company's presence in the agricultural chemical space, notably the European and North American regions, enabled it to build a respectable industry position. Since being acquired by FMC, Cheminova's products have been folded into FMC's larger product lineup, creating a more diversified product line.

Lemax Chemical Co., Ltd.: (5-8%)

Lemax Chemical Co., Ltd. has earned a reputation of its own as a leading contributor in the Chinese landscape and specifically within Asia in the industry. Despite its lower share in comparison to the world leaders Adama and UPL, Lemax enjoys its concentration on specialty chemical use and low-price strategy.

The capacity of the company to supply both the domestic and foreign industries with cost-efficient solutions has helped it to be competitive in this segment. Lemax product lines find their relevance most strongly for small-scale agricultural producers as well as industrial users, where pricing and versatility are key considerations.

Other Key Players

- Ratnamani

- Novasep

- Arkema

- Otto Chemie Pvt. Ltd.

- BASF SE

- Syngenta AG

- Corporation

- Dow Chemical Company

- Corteva Agriscience

- Bayer AG

- Monsanto Company

Segmentation

-

By Form :

- Solid

- Liquid

-

By Grade :

- >98%

- <99%

-

By End Use :

- Agrochemical

- Pharmaceutical

- Others

-

By Region :

- North America

- Latin America

- Europe

- Asia Pacific

- Middle East and Africa (MEA)

- Frequently Asked Questions -

How big is the triazole market?

The industry is anticipated to reach USD 810.1 million in 2025.

What is the outlook on triazole sales?

The industry is predicted to reach a size of USD 1,251.9 million by 2035.

Who are the key triazole companies?

Prominent players include Ratnamani, Novasep, Arkema, Otto Chemie Pvt. Ltd., BASF SE, Syngenta AG, Dow Chemical Company, Corteva Agriscience, Bayer AG, Monsanto Company, and others.

Which form of triazole is widely used?

The liquid form is widely used.

Which country is likely to witness the fastest growth in the triazole market?

China, set to grow at 5.4% CAGR during the forecast period, is poised for the fastest growth.

Author:

S.N. Jha

Editor:

Naved Ahmed